The Drift Curve

Britain took twenty years to lose its car industry. Sweden took three. Germany does not have either amount of time.

Cost accelerates before anyone chooses to see it.

In 2008 I sat inside Saab Automobile's global headquarters as General Motors' appointed lead for separating the company from its parent, coordinating the split across every GM region and national sales company worldwide. Sweden's automotive industry was coming apart, and my job was to manage the mechanics of its dismantling.

One decision from that period still captures the second stage of this pattern better than any balance sheet could. Around that same time, GM took the Saab 9-3, kept the platform, the engines, and the production line in Trollhättan almost entirely intact, and sold it in Europe as a Cadillac. Internally, people at Saab called it the Bob Lutz Special, after the GM executive who championed it. It sold roughly 7,400 units over its lifetime, in a market GM had hoped would rival the BMW 3 Series and Mercedes C-Class. That is not a company fighting for its future. That is a parent so confident in its own position that a shortcut looked like a reasonable bet. It is what complacency looks like from inside a boardroom, and it is exactly the second stage of the pattern this piece is about to name.

Saab did not survive it. Volvo did, sold to Geely in 2010, the first time a Chinese manufacturer acquired a live, functioning, premium European brand outright rather than picking up the pieces of a bankruptcy.

I later spent a decade at Jaguar Land Rover, including as the company's European lead for Brexit contingency planning, watching a different version of the same pattern from inside Britain. MG was sold out of bankruptcy to a Chinese buyer in 2005. Vauxhall survives today as a badge with no independent industrial substance. Sunderland, once the proof that Britain could still build cars at scale, is now running at under half its installed capacity and has signed an agreement to explore building Chinese cars on its own lines. Britain's collapse took roughly twenty years to run its course.

Two very different countries. Two very different timelines. The same underlying pattern both times, and this series is about that pattern across European automotive as a whole, not any one country in isolation.

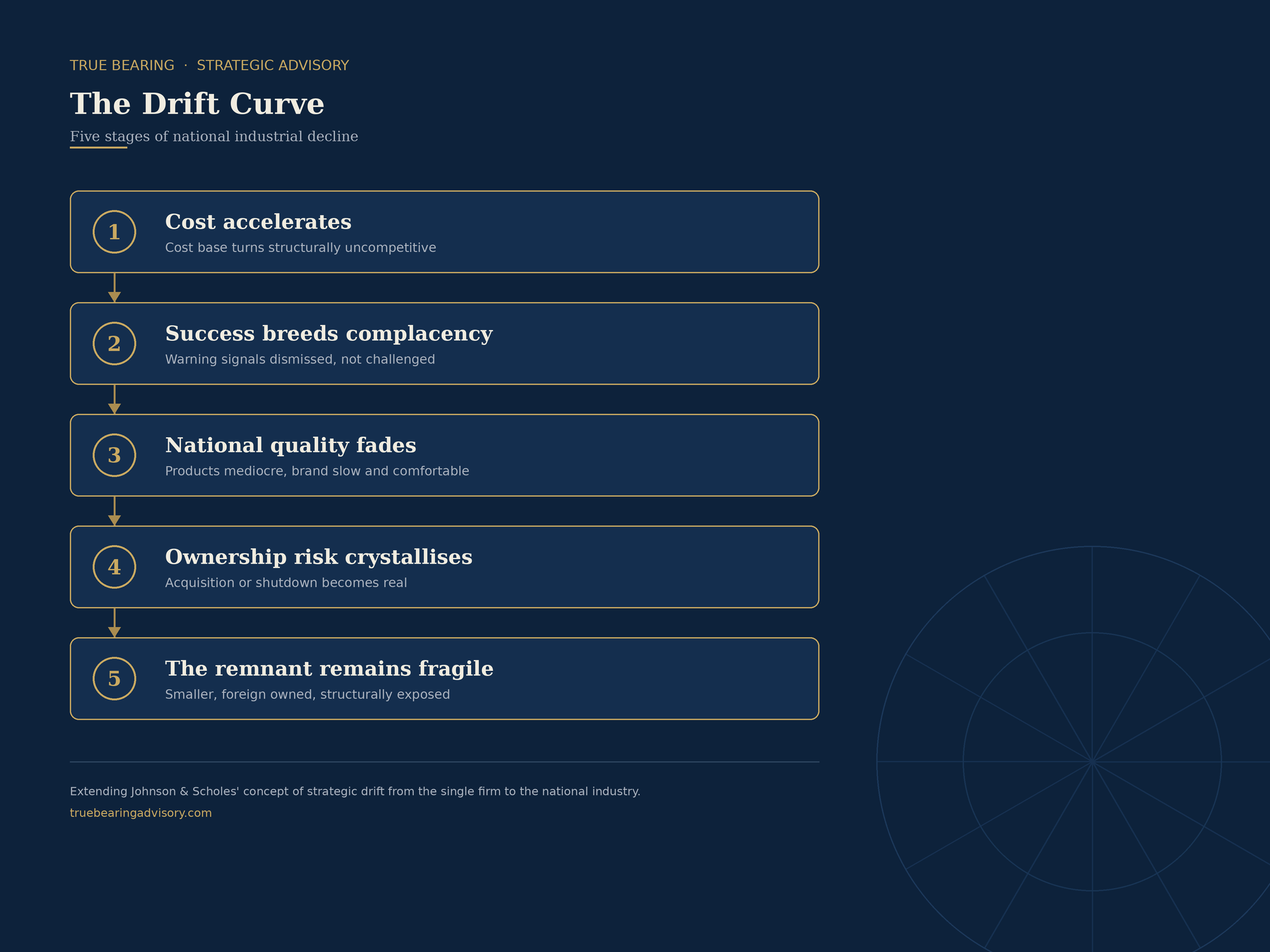

The Drift Curve — five stages, extending Johnson & Scholes' concept of strategic drift from the single firm to the national industry.

Cost accelerates first. The domestic cost base stops being competitive against global rivals, faster than the organisation can restructure around it. Success then breeds complacency, the Cadillac BLS in one sentence. National quality fades next, as products turn mediocre and brands turn slow and comfortable, until the country's own reputation for quality starts working against the industry instead of for it. Ownership risk then crystallises, and acquisition, carve-out, or shutdown moves from a hypothetical to a live boardroom conversation. What happens after that splits three ways depending on where a brand sits. The rarest, most bespoke names often thrive under new capital. The broad middle tier stays exposed no matter how deep the new owner's pockets are. True volume manufacturing, the plants building hundreds of thousands of ordinary cars a year, tends to disappear outright.

This extends an idea from strategy theory usually applied to a single company. Johnson and Scholes described it in 1988 as strategic drift, the gradual loss of fit between an organisation's strategy and its environment. Britain and Sweden show the same mechanism operating at the level of an entire national industry.

None of this happened in a vacuum, and it is not happening in one now. While Britain and Sweden were working through their own internal versions of this pattern, they had the relative luxury of time, because nobody outside was actively accelerating the collapse. That is no longer true. Chinese manufacturers are currently mounting a direct offensive on exactly the volume segment already under the most pressure, undercutting on price while European brands are still working out how to compete on cost at all. Sunderland's talks with Chery are not an isolated British story, they are one visible instance of a continent-wide price war that is compressing the timeline for everyone. This is not why the drift began in Germany. It is why it will not take Germany anywhere close to twenty years.

Germany's numbers today read like an industry already two years into the same five stages, moving through the first three simultaneously. Job losses already in the tens of thousands, with forecasts running into six figures over the next decade. Plants closing or being offered to defence manufacturers instead of car buyers. And the quality signal is already moving. In the most recent independent U.S. vehicle dependability rankings, Audi finished as the lowest-rated premium brand of any nationality on earth, Mercedes sat in the bottom ten of the entire industry, and Volkswagen dropped to second from last the following year. The one clean exception was Porsche, which finished third among all premium brands two years running, a brand insulated by scarcity and price in exactly the way this series will keep coming back to.

Diagnostics, not prophecy. Direction first, then movement.

This is not a claim that Germany will end up where Britain or Sweden did. The five stages are a diagnostic, not a forecast. They raise the probability of a particular outcome and create urgency around the decisions that still separate one path from another. Neither Britain's story nor Sweden's had to end the way it did. Germany's does not either, and unlike either of them, Germany has a genuine collective option neither country had available, at a moment when a genuine external competitor is actively working to close that window faster than either historical case ever experienced.

Over the next six weeks this series works through where the pattern leads across European automotive. The OEMs caught between a shrinking premium tier and a collapsing volume market, and the very different bets VW, Stellantis, and Renault are placing on survival. The suppliers who pay the direct price for decisions made above them. The brand economics that actually decide who keeps their margin, and why flooding the market on price alone is not a strategy China's own manufacturers can sustain either. The dealer networks absorbing the indirect cost of every decision made upstream. The financing question underneath all of it. And finally, whether "Made in Europe" can be the continent's way off the curve.

If this pattern is already playing out inside your own organisation, market, or portfolio, I'd welcome the conversation. truebearingadvisory.com

Balázs Roóz

Founder, True Bearing Advisory

Strategic Advisory · Munich & Limassol